insight

AAM Corporate Credit View: April 2011

April 8, 2011

Will Higher Commodity Prices Result in Wider Spreads?

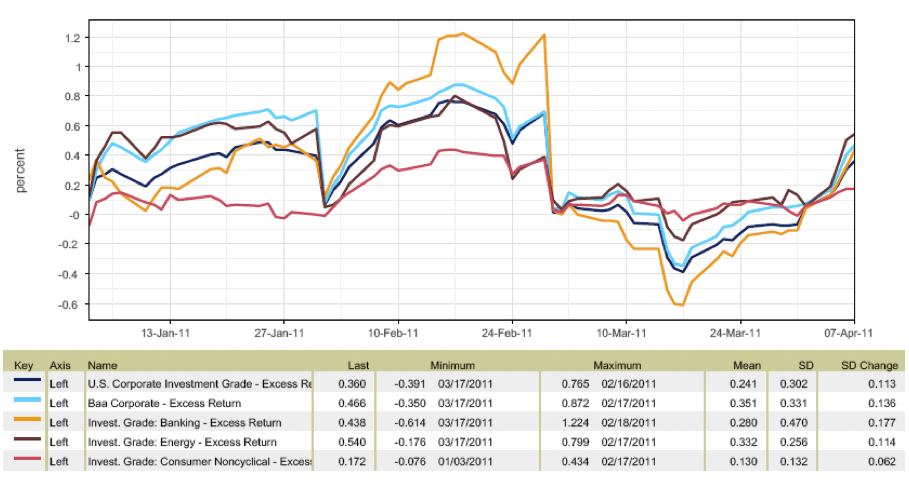

Spreads widened in March, as we had expected, but have rebounded sharply to date in April. The Barclays Corporate Index generated -6 basis points (bps) of excess return in March, getting as low as -39 bps in mid-March. From that point, spreads have tightened and excess returns are 36 bps month-to-date as of April 7. Higher beta sectors underperformed, as highlighted in Exhibit 1. We were active buyers of credits that widened more than their risk profiles would indicate, taking advantage of a more active new issue market in March.

Our outlook remains unchanged for Corporate credit, expecting outperformance in 2011 relative to Treasuries. While today’s challenges such as rising commodity costs may increase volatility and a divergence of performance among credits and sectors, we do not believe they warrant a revaluation of Corporate credit. Commodity prices remain within our “base case” and unless labor costs begin to show signs of increasing, we are not concerned about inflation in the near term. Companies are showing signs that they are able to pass through modest price increases; therefore, our expectation is for margins to remain range bound and for consumers to spend less, resulting in modest downward pressure on GDP. That said, we continue to expect modest GDP growth (3%), acknowledging that the risks are to the downside, therefore, limiting the upside.

Exhibit 1: Excess Returns Year-to-Date 2011

Source: Barclays Capital

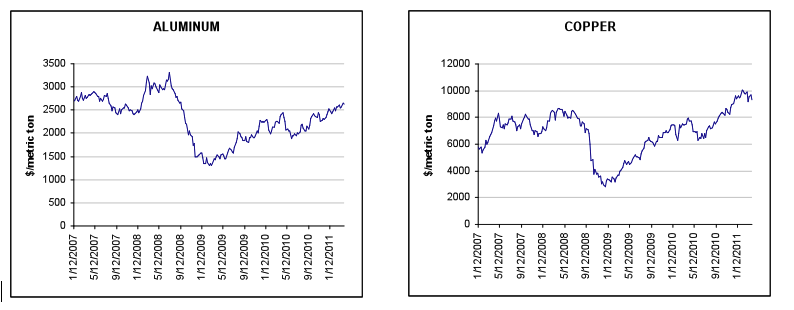

Incorporating the economic consequences of the fighting in the Middle East and the earthquake in Japan, economists revised their first quarter 2011 GDP estimate down 80 bps to 2.6%.[note]Bloomberg News – Economists surveyed from April 1, 2011 to April 7, 2011[/note] In January, we cited higher input prices as a risk to our forecast for positive excess returns for Corporates in 2011. So far this year, while they have increased, they have remained within our forecasted range. Oil continues on its upward path (see AAM Corporate Credit View dated March 7, 2011) and we will be following the elections in oil rich Nigeria this month, which could adversely affect an already tight supply situation. While gold and oil have received a lot of attention, other commodity prices have also risen sharply, approaching or exceeding their 2007 levels (Exhibit 2). Reasons for this include loose liquidity conditions, negative real rates, improving global manufacturing activity which includes the beginning of China’s twelfth five-year plan. China continues to consume more than one third of many metals, as shown in Exhibit 3. The point is since the increase in commodity prices is fundamentally driven, prices are unlikely to change course in the near term without an unexpected downward revision to economic growth in China, the United States and/or emerging markets or ramp in currently constrained supply.

Exhibit 2 Commodity Prices are Increasing

Source: Bloomberg

Exhibit 3

| Market Balance and Price Outlook | 2009 | 2010 | 2011F |

| Aluminum | |||

| China as % of total consumption | 41% | 41% | 42% |

| Surplus/(deficit) as % of total demand | 10% | 2% | 2% |

| Refined Copper | |||

| China as % of total consumption | 37% | 39% | 39% |

| Surplus/(deficit) as % of total demand | 6% | 1% | -3% |

| Primary Nickel | |||

| China as % of total consumption | 36% | 34% | 36% |

| Surplus/(deficit) as % of total demand | 3% | -3% | 1% |

| Refined Zinc | |||

| China as % of total consumption | 41% | 41% | 42% |

| Surplus/(deficit) as % of total demand | 10% | 5% | 1% |

| Iron Ore | |||

| China’s share of global trade | 67% | 62% | 62% |

| China’s iron ore import ratio | 70% | 64% | 67% |

| Surplus/(deficit) as % of total demand | 1% | 4% | 2% |

Source: CRU International; Brook Hunt; GS&PA

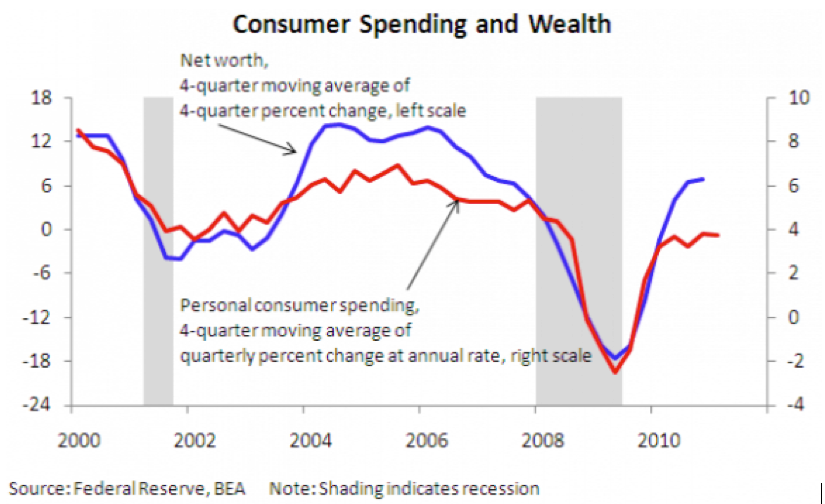

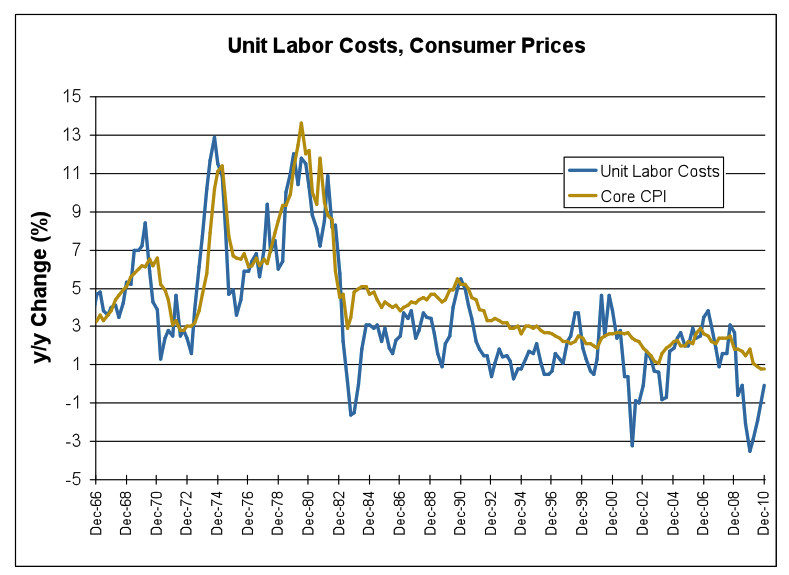

Our concern regarding higher input prices was the pressure they could place on margins if companies are unable to pass through the costs to a recovering consumer. We will glean more information soon in earnings calls, but are hearing companies have been successful at passing through price increases in small, frequent steps. While this may be supportive for company margins, we wonder how resilient the consumer will be if paychecks are eroded by higher food and energy prices while housing remains weak and unemployment remains high. Recognizing that consumer spending is tied to wealth (Exhibit 4) and that higher income households generate a proportionately higher amount of consumer spending, we are not yet concerned that such pressure will result in a double dip since the stock market is in positive territory year-to-date and home prices are falling less rapidly. In addition, the slack in the labor market and the relationship between labor costs and CPI (Exhibit 5) make us less concerned about inflation in the near term. Of course, the economy is recovering and set-backs are still possible, including the uncertainty relating to the end of the Federal Reserve’s second Quantitative Easing (QE2) program in the middle of this year. This risk, in addition to the others highlighted in this paper, concern us. But, unless the probability of a double dip begins to increase, we believe Corporate credit will outperform Treasuries in 2011.

Exhibit 4

Exhibit 5

Source: Bloomberg

Disclaimer: Asset Allocation & Management Company, LLC (AAM) is an investment adviser registered with the Securities and Exchange Commission, specializing in fixed-income asset management services for insurance companies. This information was developed using publicly available information, internally developed data and outside sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated and the opinions given are accurate, complete and reasonable, liability is expressly disclaimed by AAM and any affiliates (collectively known as “AAM”), and their representative officers and employees. This report has been prepared for informational purposes only and does not purport to represent a complete analysis of any security, company or industry discussed. Any opinions and/or recommendations expressed are subject to change without notice and should be considered only as part of a diversified portfolio. A complete list of investment recommendations made during the past year is available upon request. Past performance is not an indication of future returns.

This information is distributed to recipients including AAM, any of which may have acted on the basis of the information, or may have an ownership interest in securities to which the information relates. It may also be distributed to clients of AAM, as well as to other recipients with whom no such client relationship exists. Providing this information does not, in and of itself, constitute a recommendation by AAM, nor does it imply that the purchase or sale of any security is suitable for the recipient. Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, inflation, liquidity, valuation, volatility, prepayment and

Disclaimer: Asset Allocation & Management Company, LLC (AAM) is an investment adviser registered with the Securities and Exchange Commission, specializing in fixed-income asset management services for insurance companies. Registration does not imply a certain level of skill or training. This information was developed using publicly available information, internally developed data and outside sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated and the opinions given are accurate, complete and reasonable, liability is expressly disclaimed by AAM and any affiliates (collectively known as “AAM”), and their representative officers and employees. This report has been prepared for informational purposes only and does not purport to represent a complete analysis of any security, company or industry discussed. Any opinions and/or recommendations expressed are subject to change without notice and should be considered only as part of a diversified portfolio. Any opinions and statements contained herein of financial market trends based on market conditions constitute our judgment. This material may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or targets will be achieved, and may be significantly different than that discussed here. The information presented, including any statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Although the assumptions underlying the forward-looking statements that may be contained herein are believed to be reasonable they can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. AAM assumes no duty to provide updates to any analysis contained herein. A complete list of investment recommendations made during the past year is available upon request. Past performance is not an indication of future returns. This information is distributed to recipients including AAM, any of which may have acted on the basis of the information, or may have an ownership interest in securities to which the information relates. It may also be distributed to clients of AAM, as well as to other recipients with whom no such client relationship exists. Providing this information does not, in and of itself, constitute a recommendation by AAM, nor does it imply that the purchase or sale of any security is suitable for the recipient. Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, inflation, liquidity, valuation, volatility, prepayment and extension. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.