insight

AAM Corporate Credit View: October 2010

October 6, 2010

How Should I Spend My Cash?

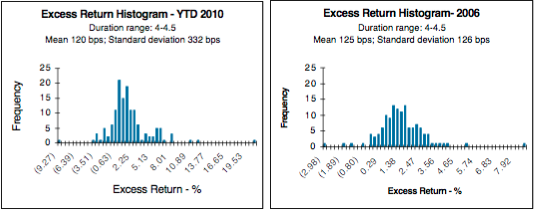

While not as strong as the equity market, the investment grade credit market as represented by the Barclays Corporate Bond Index posted positive excess returns in September (78 basis points (bps)). This returns the Index, once again, to positive territory for the year (39 bps). Despite the positive excess returns in 2010, idiosyncratic (firm specific) risk remains high, as reflected by the histograms in Exhibit 1. Although the means of excess returns from 2010 and 2006 are approximately the same, the volatility is almost three times greater so far in 2010. The outperformers in 2010 have been primarily finance credits, while the underperformers reside in many different industries. We expect idiosyncratic risk to remain high for the next 12-18 months and anticipate companies to become more active with their large cash coffers. Unlike 2009-2010, where sector/industry selection was key for outperformance, we expect credit selection and the ability to wait for new issues will be the keys for outperformance going forward.

Many economists are citing the large cash balances on company balance sheets as a source for economic stimulus. We believe the peak of the cash balances may be the second half of 2010. After the setback experienced in the second quarter of 2010, consensus seems to be forming around a slow growth economic environment. The probability of a double dip varies depending on the economist, but even a bear like Dr. Nouriel Roubini is assigning a 40% chance compared to others that are in the 20-33% range. The Federal Reserve’s recent actions and comments also serve to reduce the economic uncertainty. This leaves regulatory and political uncertainty, acting as implicit costs for companies.

In this environment of low growth and political sensitivity towards the economy, we expect companies will start spending their cash. That said, we expect the cash to be spent primarily on the following in lieu of growth related investments which would provide more of a catalyst for hiring (not in any particular order):

- Capital spending related to productivity enhancements

- Repurchasing shares and/or debt

- Increasing or initiating dividends

- Mergers and acquisitions (M&A)

Technology related companies are among those that have benefited from the investment in productivity. For instance, in its recent investor meeting, Kroger, a retail supermarket chain, commented that its current capital expenditure strategy continues to focus on projects that will either help drive improvement in sales productivity or costs versus spending on new development.

We expect more companies to make announcements relating to share repurchases or increased dividends. Cisco, a global technology company, was not alone in its plan to issue the company’s first dividend. Companies have also been active in tendering for short maturity, high coupon, or structurally superior debt or using cash to retire maturing debt in lieu of refinancing. This is being reflected by the banks as well, with corporations reducing their revolving credit facilities. Total commercial and industrial loans outstanding for the U.S. banking system fell 23% from January 2009 through August 2010, while the amounts drawn under the revolvers fell from 42% to 35% during the same time period.

Lastly, mergers and acquisitions (M&A) appear to be picking up after companies paused in the second quarter of 2010 to assess the sovereign and economic risk (Exhibit 2). Given the backdrop of low economic growth, we expect the M&A pace to accelerate as regulatory and political uncertainty decreases. Most sectors are participating in M&A for consolidation benefits relating to synergies, as opposed to investing in revenue growth opportunities.

At an equity telecommunications/media conference in late September, Verizon’s CEO, Ivan Seidenberg, stated he expected another consolidation wave over the next three to five years among content, cable, and telecommunications companies given the overcapacity. At this same conference, AT&T’s CEO, Randall Stephenson, was more positive towards M&A after shying away earlier this year given the regulatory risk. Although this is one industry that is ripe for consolidation, such M&A could lead to spread widening due to cash deals and the debt issuance and leverage that would result. Another industry that is faced with too much supply for the level of demand, in addition to heightened regulatory risk and the associated costs, is Banking. We would expect consolidation to accelerate in this sector as well via acquisitions made by both domestic and international banks. However, this is likely to be dominated by FDIC assisted deals in the near term.

Although good for the long term, these activities are first, not conducive to job growth in the near to intermediate term and second, will likely face mixed reactions from investors and rating agencies as not all will be creditor friendly. Debt issuance relating to M&A should be readily absorbed as investors continue to look to investment grade credit as a defensive investment alternative. As companies deplete their cash coffers, we expect investments to be made within current rating parameters. However, this lessens financial strength and flexibility in an environment where the risk of a double dip is not miniscule. For companies that are cyclical and have volatile cash flows, fixed income investors should be cautious of management teams that are too aggressive at this stage of the recovery.

This information is developed using publicly available information, internally developed data and outside sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated and the opinions given are accurate, complete and reasonable, liability is expressly disclaimed by AAM and any affiliates (collectively known as ‘AAM’), and their respective officers and employees. Any opinions and/or recommendations expressed are subject to change without notice.

This information is distributed to recipients including AAM, any of which may have acted on the basis of the information, or may have an ownership interest in securities to which the information relates. It may also be distributed to clients of AAM, as well as to other recipients with whom no such client relationship exists. Providing this information does not, in and of itself, constitute a recommendation by AAM, nor does it imply that the purchase or sale of any security is suitable for the recipient.

Disclaimer: Asset Allocation & Management Company, LLC (AAM) is an investment adviser registered with the Securities and Exchange Commission, specializing in fixed-income asset management services for insurance companies. Registration does not imply a certain level of skill or training. This information was developed using publicly available information, internally developed data and outside sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated and the opinions given are accurate, complete and reasonable, liability is expressly disclaimed by AAM and any affiliates (collectively known as “AAM”), and their representative officers and employees. This report has been prepared for informational purposes only and does not purport to represent a complete analysis of any security, company or industry discussed. Any opinions and/or recommendations expressed are subject to change without notice and should be considered only as part of a diversified portfolio. Any opinions and statements contained herein of financial market trends based on market conditions constitute our judgment. This material may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or targets will be achieved, and may be significantly different than that discussed here. The information presented, including any statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Although the assumptions underlying the forward-looking statements that may be contained herein are believed to be reasonable they can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. AAM assumes no duty to provide updates to any analysis contained herein. A complete list of investment recommendations made during the past year is available upon request. Past performance is not an indication of future returns. This information is distributed to recipients including AAM, any of which may have acted on the basis of the information, or may have an ownership interest in securities to which the information relates. It may also be distributed to clients of AAM, as well as to other recipients with whom no such client relationship exists. Providing this information does not, in and of itself, constitute a recommendation by AAM, nor does it imply that the purchase or sale of any security is suitable for the recipient. Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, inflation, liquidity, valuation, volatility, prepayment and extension. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.