insight

CMBS 2.0 – Not Quite the Improvement We Were Hoping For

December 21, 2011

Commercial mortgage backed security issuance has rebounded dramatically since the depths of the financial crisis. While many of the egregious lending practices of the past have been rectified, there are elements of recent transactions that pose risks to investors.

The Commercial Mortgage Backed Securities (CMBS) market underwent a rapid transformation from late 2009 through 2011, growing from a market of small, single borrower deals to larger, multiple borrower transactions. Strong demand for these deals, “CMBS 2.0” as they are popularly known, from both traditional and non-traditional participants, helped restore vibrancy and liquidity to the marketplace following the collapse of issuance in 2008. Despite increases in origination volume and transaction size over the past two years, CMBS 2.0 deals can be characterized as having relatively few underlying loans as well as lacking diversification in both underlying property type and geographic location. In addition, the original conservative underwriting standards prevalent in the first few transactions issued in 2009 have given way to aggressive origination practices, which has led to loans with lower debt service coverage ratios (DSCR) and higher loan to value ratios (LTV), and, to a lesser extent, include some pro forma underwriting. We believe that at current yield spreads, investors are not fully compensated for the risk and volatility that is inherent in these new deals.

The first newly issued CMBS transaction, following the collapse of the structured securities market, occurred in November of 2009 after a nearly two year hiatus. This initial transaction was backed by a single loan covering a small collection of retail properties made to one borrower, Developers Diversified Realty (DDR). Given that the trauma of the financial crisis was fresh in investor’s minds, the underlying loan had very conservative lending metrics with a DSCR of 2.04x and an LTV of just 51.7%. This transaction was extremely well received and based upon this positive market feedback, loan originators again began extending credit to developers for securitization in future CMBS transactions. These new CMBS 2.0 transactions quickly evolved into more traditional conduit deals backed by multiple loans, covering several different property types made to a variety of lenders. The quality of the underlying loans remained quite strong as these early securitizations were backed by loans with credit metrics very similar to the DDR deal.

While the initial credit metrics were strong, the CMBS 2.0 transactions had much greater loan concentration due to the size of the loans and the relatively small number of loans backing each transaction. The average 2007 securitization contained 200 loans averaging less than $10 million per loan while the new securitizations contained only 30 to 50 loans and averaged $30 million per loan. As a result, the top ten loans in a CMBS 2.0 transaction make up a disproportionate percentage of each deal. Historically, the top ten loans in transactions issued between 2004 and 2007 period made up between 30% and 45% of the underlying pool, while the top ten loans for deals underwritten in 2010 and 2011 averaged 69% and 62% of the pool respectively. This concentration increases the overall risk of the pool as the default of a single loan will have a dramatic impact on the overall credit performance of a securitization.

CMBS 2.0 transaction also lack diversified property types. Retail properties and office buildings comprise approximately 50% and 30%, respectively, of the underlying collateral pools. A large portion of these are located in tertiary locations such as regional malls and suburban office buildings. The tenants in secondary locations may not be as financially strong as those in primary central business districts and the time and cost to replace a tenant in the event of a vacancy can be much more difficult and expensive.

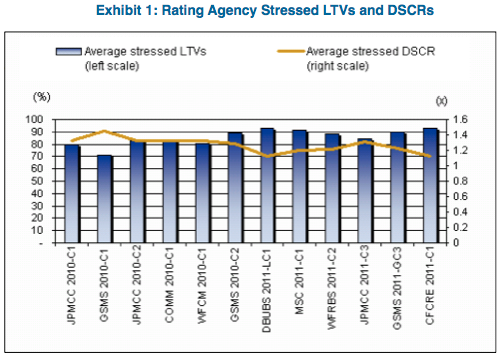

Evaluating these concentration risks becomes especially important as increased competition among lenders has led to a loosening of underwriting standards. Exhibit 1 presents the declining average DSCR and increasing LTV ratio in recent CMBS 2.0 transactions. The rating agency stressed DSCR for GSMS 2010-C1 A2 (issued in 2010) was 1.45x, and the stressed LTV was 70.8%, as compared to an average for all transactions issued in 2011 of 1.24x and 90.6%, respectively. While this trend is troublesome, these metrics still compare favorably to the averages at the market peak in 2007 when stressed DSCR averaged 0.98x and stressed LTV averaged 110.6%.

Interestingly, interest only loans are becoming more prevalent, constituting approximately 21% of newly originated CMBS transactions. The lower debt service costs of an interest only loan make DSCR appear to be more conservative but in reality mask the risk in the underlying collateral pool. The lack of principal repayments during the term of the loan makes them more difficult to refinance at maturity leading to increased default risk.

Current underwriting trends in CMBS 2.0 transactions are troubling. Collateral pools concentrated in a relatively few regional malls and suburban office parks make these securitizations particularly risky. In the event of another broad based downturn in the commercial real estate market, the concentration in these securitizations make them much more vulnerable to credit downgrade and to principal losses on lower rated classes. Had the conservative underwriting standards of the first few transactions issued in 2010 been maintained, the risks would be manageable, however in light of the erosion of those standards, we feel that the return potential is not sufficient to offset the risks. As long as senior securities are offered with yields that are comparable to government guaranteed GNMA project loans, we’ll choose to avoid this sector for now.

Mohammed Z. Ahmed

Assistant Vice President

Structured Products Analyst

For more information, contact:

Joel B. Cramer, CFA

Director of Sales and Marketing

joel.cramer@aamcompany.com

Greg Curran, CFA

Vice President, Business Development

greg.curran@aamcompany.com

Disclaimer: Asset Allocation & Management Company, LLC (AAM) is an investment adviser registered with the Securities and Exchange Commission, specializing in fixed-income asset management services for insurance companies. This information was developed using publicly available information, internally developed data and outside sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated and the opinions given are accurate, complete and reasonable, liability is expressly disclaimed by AAM and any affiliates (collectively known as “AAM”), and their representative officers and employees. This report has been prepared for informational purposes only and does not purport to represent a complete analysis of any security, company or industry discussed. Any opinions and/or recommendations expressed are subject to change without notice and should be considered only as part of a diversified portfolio. A complete list of investment recommendations made during the past year is available upon request. Past performance is not an indication of future returns.

This information is distributed to recipients including AAM, any of which may have acted on the basis of the information, or may have an ownership interest in securities to which the information relates. It may also be distributed to clients of AAM, as well as to other recipients with whom no such client relationship exists. Providing this information does not, in and of itself, constitute a recommendation by AAM, nor does it imply that the purchase or sale of any security is suitable for the recipient. Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, inflation, liquidity, valuation, volatility, prepayment and extension. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

Disclaimer: Asset Allocation & Management Company, LLC (AAM) is an investment adviser registered with the Securities and Exchange Commission, specializing in fixed-income asset management services for insurance companies. Registration does not imply a certain level of skill or training. This information was developed using publicly available information, internally developed data and outside sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated and the opinions given are accurate, complete and reasonable, liability is expressly disclaimed by AAM and any affiliates (collectively known as “AAM”), and their representative officers and employees. This report has been prepared for informational purposes only and does not purport to represent a complete analysis of any security, company or industry discussed. Any opinions and/or recommendations expressed are subject to change without notice and should be considered only as part of a diversified portfolio. Any opinions and statements contained herein of financial market trends based on market conditions constitute our judgment. This material may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or targets will be achieved, and may be significantly different than that discussed here. The information presented, including any statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Although the assumptions underlying the forward-looking statements that may be contained herein are believed to be reasonable they can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. AAM assumes no duty to provide updates to any analysis contained herein. A complete list of investment recommendations made during the past year is available upon request. Past performance is not an indication of future returns. This information is distributed to recipients including AAM, any of which may have acted on the basis of the information, or may have an ownership interest in securities to which the information relates. It may also be distributed to clients of AAM, as well as to other recipients with whom no such client relationship exists. Providing this information does not, in and of itself, constitute a recommendation by AAM, nor does it imply that the purchase or sale of any security is suitable for the recipient. Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, inflation, liquidity, valuation, volatility, prepayment and extension. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.