Overview

Environmental, social, and governance (ESG) advancement has been a prominent topic from energy management teams over the past six months. This is particularly true as it relates to environmental concerns. Politicians, scientists, and investors are shaping the future of the energy industry through increased regulation, cleaner innovation, and more expensive financing – all of which are determining capital allocation decisions by management teams in the energy industry. Recognizing this, AAM is highlighting its environmental risk analysis for energy companies. Below we identify why environmental concerns – particularly greenhouse gases (GHG) – now have the interest of energy companies and provide a framework for how we incorporate GHG emissions in our evaluation of issuers. We also provide a brief background on the key contributors to GHGs.

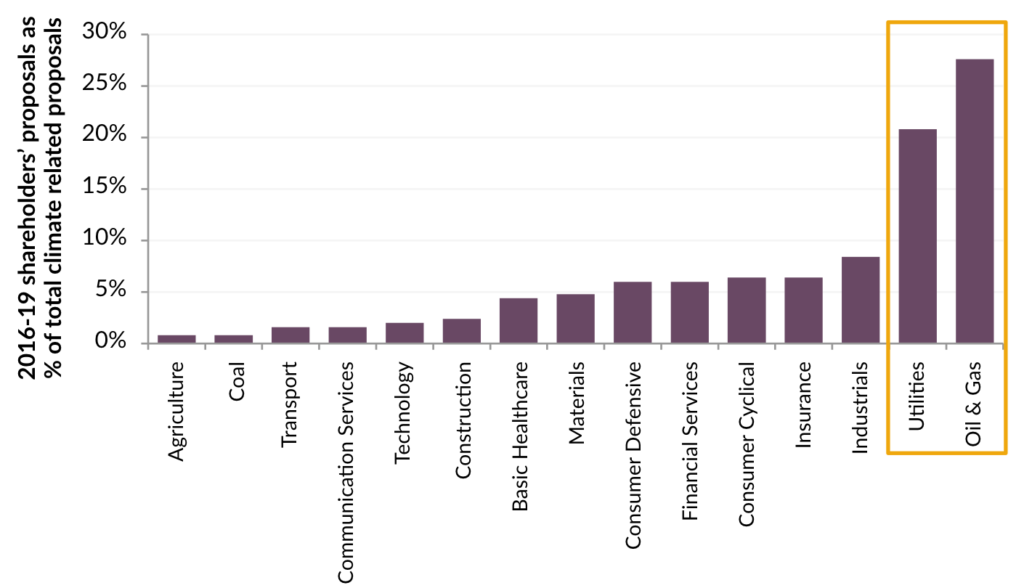

Presently, ESG efforts are affecting companies in the energy sector primarily via shareholder proposals. According to ProxyInsight and Goldman Sachs, the number of climate-related shareholder proposals has almost doubled since 2011, and the percentage of investors voting in favor has tripled over the same time period. Critically, investor pressure has been concentrated on the energy sector. Exhibit 1 shows 50% of all shareholder proposals target the energy producers (oil & gas, utilities, coal). These proposals include items such as linking executive pay to GHG emission reduction goals (Royal Dutch Shell, 2018).

Additionally, we believe conventional asset managers are increasingly under pressure to adhere to sustainable investing, which will put pressure on energy companies to improve their ways or risk losing large shareholders. We believe some of the largest asset managers will be inclined to vote against management and board directors when companies are not making sufficient progress on carbon emission disclosures.

Exhibit 1: Split of climate-related shareholder proposals, 2016-2019 average, by industry

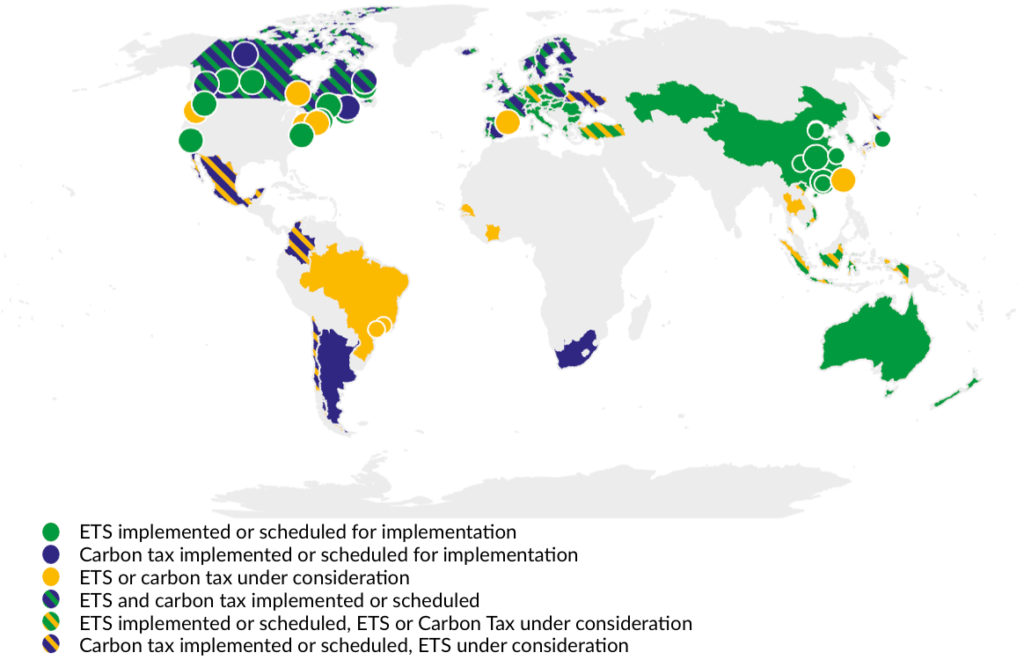

We are also mindful that environmental concerns could negatively affect cash flow in the intermediate term. According to the World Bank, carbon prices have already been implemented in 40 countries (see Exhibit 2 below). Provided that several candidates running for the U.S. Presidency are open to a carbon tax or carbon pricing via an electronic trading system (ETS), we believe that at some point in the intermediate term, energy companies in the U.S. will be subject to carbon costs too.

Exhibit 2: Summary map of regional, national, and subnational pricing initiatives

Energy analysis: focusing on the E in ESG

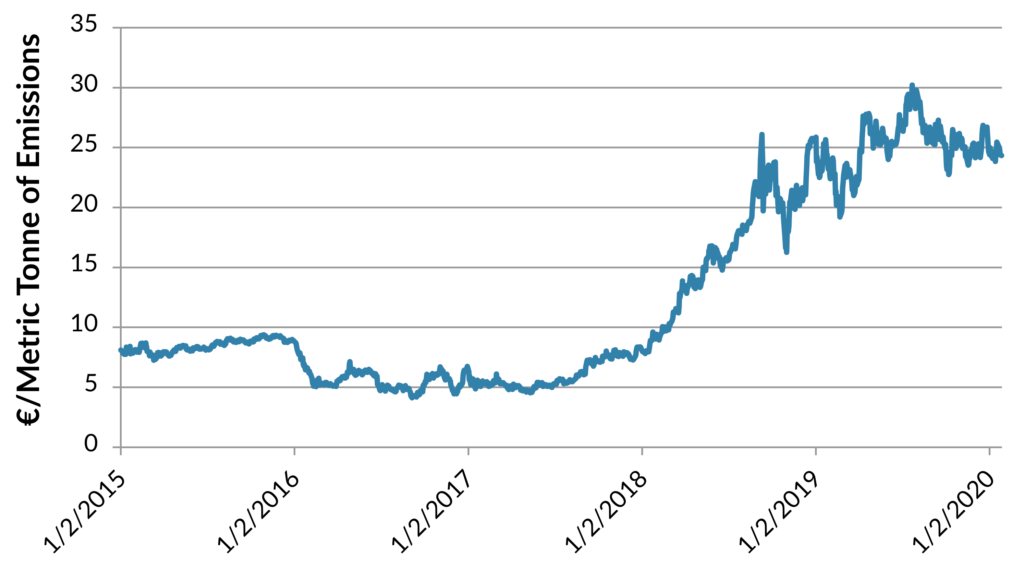

AAM has incorporated many aspects of sustainable investing for years. One item that has evolved in the past decade is the analysis of carbon emissions in the energy sector. To quantify how carbon restrictions might effect energy companies in the investment grade index, we assume a mechanism will be employed in the U.S. similar to that used in Europe where emitters can trade emission units to meet their emission targets. To comply with their emission targets at the lowest cost, entities can either implement internal reduction measures or acquire emission units in the carbon market, depending on the relative costs of these options. By creating supply and demand for emissions units, an electronic trading system establishes a market price for GHG emissions as is done presently in Europe. (Exhibit 3). We acknowledge that there is disagreement over whether such a policy will be implemented in the U.S., and, if so, how it will be implemented (trading system or explicit tax). However, we attempt to quantify the risk each issuer has to carbon costs and evaluate energy companies potential exposure to a change in U.S. legislation.

Exhibit 3: ICE EU active carbon emissions

GHG analysis in AAM’s risk assessment

We use two primary sources to determine GHG emissions: company sustainability reports and the U.S. Environmental Protection Agency (EPA) Greenhouse Gas Reporting Program. The integrated companies, Canadian issuers, and independent companies with international exposure generally post GHG emissions in their sustainability reports. The other primarily domestic energy companies are required to report GHG from sources that in general emit 25,000 metric tons or more of carbon dioxide equivalent per year in the United States.

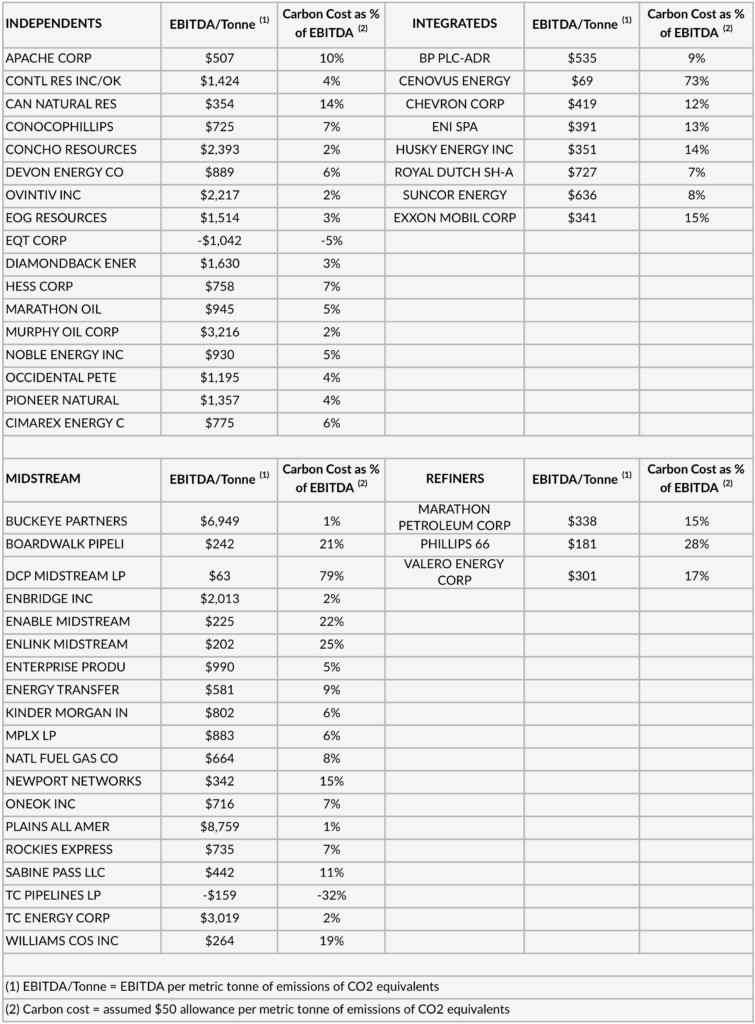

In addition to the traditional factors we already use in assessing the risk of an energy issuer, we include two environmentally-related items: a.) EBITDA per metric tonne of GHG emissions, which indicates how much cash flow the issuer generates for every tonne of emissions and b.) implied carbon costs as a % of EBITDA, which measures the percentage of cash flow a theoretical carbon tax of $50 per tonne would be. All other factors being equal, an issuer with high EBITDA per metric tonne of GHG emissions and low carbon costs as a % of EBITDA has a better internal risk rating. Exhibit 4 includes these AAM risk measures for the energy issuers included in the Bloomberg Barclays Index.

Exhibit 4: Cash flows in relation to carbon costs

The challenges to measuring environmental impacts

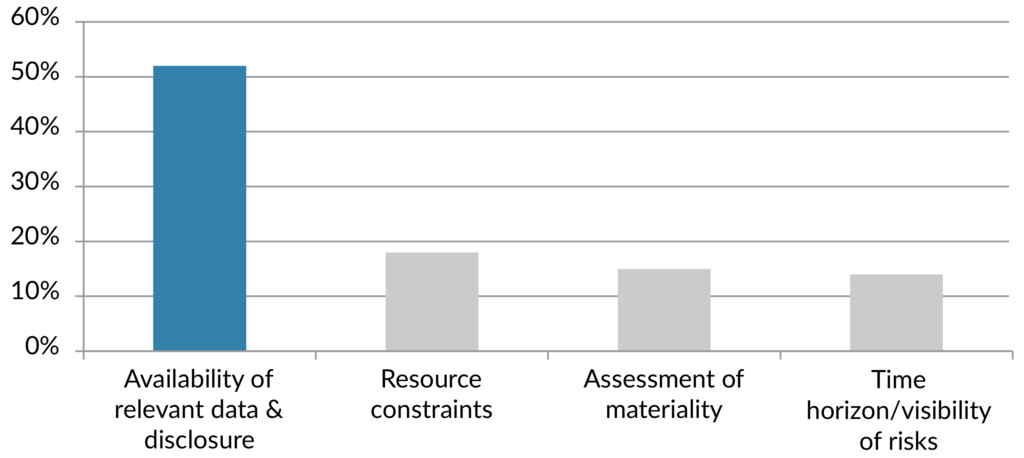

Unfortunately, we observe two challenges when evaluating the environmental impact of energy companies. First, there is no consistency on whether the issuers actually report an environmental impact statement. Moreover, if there is an impact statement there is no standard on how the information is reported or what the benchmark is. (The one item that has been standardized and is widely identified is GHG emissions, which is why we are focusing on this data rather than on other environmental impact items such as energy consumption, pipeline spills, water consumption or methane flaring ). The second challenge is that the figures included in the environmental impact statement and/or included in the EPA database are submitted by the emitter and do not require third party verification. In a recent poll taken by Moody’s, this lack of data integrity was the overwhelming challenge to integrating ESG considerations into credit risk (see Exhibit 5).

Exhibit 5: Greatest challenge to integrating ESG considerations into credit risk

The key GHGs and the human activities behind them

What makes reducing GHG so difficult is that many of the activities we take for granted and are very reluctant to give up – like driving or using air conditioning – contribute to increased GHG emissions. Gases that trap heat in the atmosphere are called GHGs. The main GHGs are carbon dioxide, methane, and nitrous oxide. The international standard practice is to express GHGs in carbon dioxide equivalents. Emissions of gases other than carbon dioxide are translated into carbon dioxide equivalents using global warming potential.

Carbon dioxide is by far the largest GHG emitted by human activities at about 82% of the total. The EPA states that the main human activity that emits carbon dioxide is the combustion of fossil fuels (coal, natural gas, and oil) for energy and transportation. Although, certain industrial processes and land-use changes also emit the gas.

The next largest GHG is methane at about 10% of the total. However, methane is more efficient at trapping radiation than carbon dioxide. According to the EPA, the comparative impact of methane is more than 25 times greater than carbon dioxide over a 100-year period and explains why reducing methane leakage is so critical to GHG reduction. Natural gas and petroleum systems are the largest source of methane emissions in the United States.

Nitrous oxide is the other major GHG. It is responsible for about 6% of GHG emissions from human activities. The application of nitrogen fertilizers accounts for the majority of nitrous oxide emissions in the United States.

Implications of ESG on the energy sector

GHG reduction efforts are contributing to more labor and capital devoted to non-natural resource extraction activities by the energy sector. We expect this flow of resources to accelerate in the near term, reducing the amount of capital available for traditional expenditures like exploration, acquistions, and/or development. This, combined with a lack of free cash flow and challenging macroeconomic conditions in recent years, has contributed to tight financial conditions and a relatively high cost of capital for the energy sector. We expect the supply of hydrocarbons like crude oil and natural gas to be negatively affected by increased decarbonization efforts in the intermediate term.

Additionally, the GHG reduction focus has been on the emitters who control hydrocarbon supply, as opposed to the industries or activities that consume hydrocarbons. Unless there are similar efforts to reduce fossil fuel consumption (less transportation, reduced electricity consumption, etc.), demand will continue to rise. We believe this combination of lower supply and steady demand growth to eventually eat through the excess inventory available and lead to higher crude oil and natural gas prices.

Until that time though, we expect energy companies to face familiar challenges – volatile commodity prices, displeased shareholders and, expensive access to capital. Adhering to comparatively high environmental demands along with these other items justifies the sector trading at a discount to similar rated non-energy industrials.

Disclaimer: Asset Allocation & Management Company, LLC (AAM) is an investment adviser registered with the Securities and Exchange Commission, specializing in fixed-income asset management services for insurance companies. Registration does not imply a certain level of skill or training. This information was developed using publicly available information, internally developed data and outside sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated and the opinions given are accurate, complete and reasonable, liability is expressly disclaimed by AAM and any affiliates (collectively known as “AAM”), and their representative officers and employees. This report has been prepared for informational purposes only and does not purport to represent a complete analysis of any security, company or industry discussed. Any opinions and/or recommendations expressed are subject to change without notice and should be considered only as part of a diversified portfolio. Any opinions and statements contained herein of financial market trends based on market conditions constitute our judgment. This material may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or targets will be achieved, and may be significantly different than that discussed here. The information presented, including any statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Although the assumptions underlying the forward-looking statements that may be contained herein are believed to be reasonable they can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. AAM assumes no duty to provide updates to any analysis contained herein. A complete list of investment recommendations made during the past year is available upon request. Past performance is not an indication of future returns. This information is distributed to recipients including AAM, any of which may have acted on the basis of the information, or may have an ownership interest in securities to which the information relates. It may also be distributed to clients of AAM, as well as to other recipients with whom no such client relationship exists. Providing this information does not, in and of itself, constitute a recommendation by AAM, nor does it imply that the purchase or sale of any security is suitable for the recipient. Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, inflation, liquidity, valuation, volatility, prepayment and extension. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.